🌊 Will the Bubble Ever Burst?

The evidence that suggests we are – and aren’t – headed to a new financial disaster

Nvidia invests up to $100B in OpenAI. In return, OpenAI commits to buy huge volumes of Nvidia chips.

Meanwhile, OpenAI strikes a multibillion-dollar chip deal with AMD and gets the rights to acquire up to ~10% of AMD’s stock.

And don’t forget, OpenAI has committed to a $300B compute/infrastructure deal with Oracle, building data centers that will be stuffed with chips (some of which are from Nvidia or AMD).

AMD and Oracle then announce they’ll deploy 50,000 of AMD’s MI450 GPUs in Oracle’s cloud/AI superclusters. So Oracle is buying AMD chips, which OpenAI partly owns.

And, of course, Nvidia is investing in AI infrastructure companies that are buying – whose? – Nvidia’s(!) hardware.

What the hell is happening in the AI industry? In the economy? In the market? No one seems to know, but deals keep getting made and stocks keep going up, up, up….

Today, we look at a few questions: Are we headed to a 2008-, 2000-, or 1929-level calamity? Are these circular deals – that nitwits like us can scarcely understand – signs that the AI bubble is bubbling up into a disaster? Or has Wall Street learned to only strike wise deals, moved on from “irrational exuberance,” and put us on the path to a financial golden age?

We examine these questions in today’s deep-dive and see what financial history tells us about our current situation.

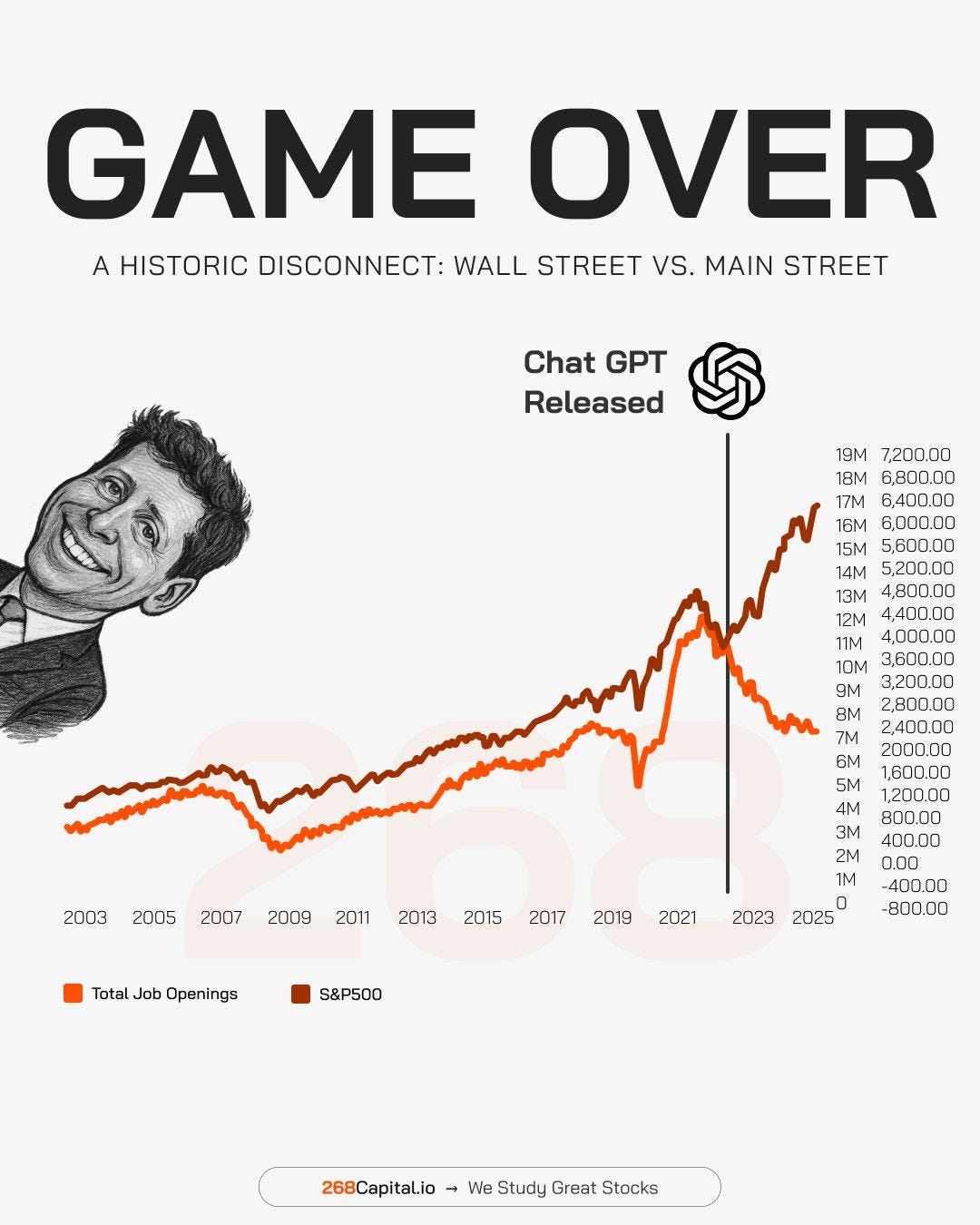

Which economy are you living in? Because right now, the US effectively has two: AI (booming) and non-AI (not booming).

Right now, there are a record 11 trillion-dollar-plus companies, four of which are worth $3T+. That’s never happened before. But almost as much as stocks are up, jobs are down. Take a look at the below chart, from the newsletter 268capital.

Yet the market is weaker than it looks: On September 29, Morgan Stanley Wealth Management’s chief investment officer released a report noting that since the AI boom began with the release of ChatGPT in November 2022, 75% of S&P 500 returns and 80% of S&P 500 profit growth have come from “AI data center-ecosystem stocks.” She noted that high stock returns over the past three years have been a “one-note narrative.” In other words: Almost totally dependent on AI.

Wherever you look right now, money is rushing to AI. One successful tech entrepreneur recently told me that if he put “.ai” at the end of his company, his accounts would have another zero at the end. Statements like this are commonplace and backed up by the money: Just this week, a Financial Times analysis found that the ten largest AI startups have seen their collective valuations increase by roughly $1T in the last 12 months. For context, in 2010, the US had only 33 startups that were each worth over $1B.

The biggest winners of the FT’s analysis were OpenAI – whose valuation has gone from ~$80B to $500B in a year; xAI ($25B to $200B); Anthropic ($20B to $180B); and Databricks ($45B to $100B).

The FT compared the situation to two prior bubbles, the dot-com boom in 2000 and the software bubble in 2021. It found that we are in uncharted territory:

The current scale of investment is of a different magnitude. VCs [venture capital firms] invested $10.5bn into internet companies in 2000, roughly $20bn adjusted for inflation. In all of 2021, they put $135bn into software-as-a-service start-ups, according to PitchBook. VCs are on course to spend well over $200bn on AI companies this year.

The chief executive of General Catalyst, one of the largest VC firms, told the paper that we’re undeniably in a bubble: “Of course there’s a bubble…Bubbles are good. Bubbles align capital and talent in a new trend, and that creates some carnage but it also creates enduring, new businesses that change the world.”

Not all agree.

Analysts are scouring history for parallels to this current moment.

Some have settled on 2008, when complex financial maneuvers created a housing market bubble that popped and brought financial markets down with it. Others have looked at 1929, when hype around new technology – the radio! – sent shares of Radio Corporation of America from $1.50 to $85.50 in just seven years. The Nvidia of the 1920s, except it then plummeted.

But perhaps the most obvious comparison is 2000, when the internet was about to change everything – and no one wanted to miss out. Like 2025, there was no doubt that the arrival of new technology was going to change things and make some people a lot of money. And, because of that, people put money into anything internet related: Pets.com raised $82M in an IPO, only to burn through the money in nine months and see its stock fall from $11 to $0.19; eToys.com was worth more than Toys “R” Us without ever making money – and went from an $8B market cap to a $5M sale within two years; theGlobe.com surged a record 606% on its IPO day, making its two founders, age 23, worth $100M+ each – only for shares to go for <$1 within two years. These were not proven businesses, but people couldn’t risk moving out.

Of course, not everything went bust: Amazon, eBay, Apple, and many other companies saw their valuations plummet – only to emerge more valuable than ever before.

What each of those bubbles – and most others, for that matter – has in common is FOMO, the fear of missing out.

In 1929, it led people to pour their fortunes into the market, only to lose everything. As a journalist at Harper’s Magazine wrote in 1931, “Stories of fortunes made overnight were on everybody’s lips…Wives were asking their husbands why they were so slow, why they weren’t getting in on all this, only to hear that their husbands had bought a hundred shares of American Linseed that very morning.”

Then in 2000, more of the same: Fear of missing out on early internet investments drove the Nasdaq up 600% between 1995 and March 2000, only to then drop 78%. The Nasdaq didn’t regain those losses until 2015.

And, of course, 2008: If you’ve seen The Big Short, you may remember the stripper telling trader Mark Baum (Steve Carell): “I have five houses and a condo.”

Baum gets on the phone: “Hey, there’s a bubble!”

FOMO is undeniably part of the current scene. No one wants to miss out on the technology that will enable companies to eliminate millions of jobs. But the question is: Is the FOMO justified?

Investors are pouring billions into these companies not because of what they are, but because of what they can be. They are drooling over getting into the next Meta or Google before it’s turned a profit – something no major AI company has done. And the promise is even greater.

The unprecedented amounts of capital flowing to the AI industry are bets on building artificial generative intelligence, or AGI. AGI, to quote ChatGPT, is “a form of artificial intelligence capable of understanding, learning, and applying knowledge across a wide range of tasks at or beyond the level of human intelligence.” It’s the technology that wouldn’t just be used by a doctor, lawyer, or receptionist – but would replace them altogether. It’s the technology that Anthropic’s CEO has warned could generate 20% unemployment within five years.

Investors are pouring their money into the companies seeking to create this, as well as the ones building out the infrastructure to do so. This explains why OpenAI is worth $500B despite losing $8B in the first half of this year, or why Elon Musk’s xAI is worth $200B while reportedly losing $1B each month and making just $200M in yearly revenue. It’s why several AI companies are worth over $10B without bringing in a single dollar. If AGI meets the hype, whoever builds it changes the world.

So are these valuations out of whack? According to a new report by the Bank of England, valuations across the US stock market are now “comparable to the peak of the dot-com bubble.” It then hedged that assessment, saying that if you look at future predicted earnings, valuations are “below the levels reached during the dot-com bubble.”

Yet future predicted earnings are just that: Predictions. They can be wrong, and if they are, how wrong they are may decide the impact of the bubble.

Leaders across the finance industry are now predicting that the market will “correct” itself in the not-too-distant future.

David Solomon, the chief executive of Goldman Sachs, recently said, “There will be a check at some point, there will be a drawdown.” JPMorgan Chase CEO Jamie Dimon said he was “far more worried” than others about a major market dip. Morgan Stanley’s Chief Investment Officer Lisa Shalett recently said she was “very concerned” about what will happen if AI does not meet expectations: “At the end of the day…this is not going to be pretty,” she said.

How ugly could it get? Predictions range from a mild downturn to a cataclysm.

In 2000, the dot-com bubble burst had a limited impact on the rest of the economy. Exposure to tech stocks was relatively limited, meaning that losses were relatively concentrated and didn’t reverberate through the rest of the economy. Wealth was destroyed on paper; less in real life.

This week, Gita Gopinath – a Harvard professor and the IMF’s chief economist from 2019 to 2022 – said the situation is currently much different, in part because global markets are now far more invested in American growth and stocks, where the AI boom is concentrated. She predicts that a downturn “could be far more severe and global in scope than those felt a quarter of a century ago,” writing, “I calculate that a market correction of the same magnitude as the dotcom crash could wipe out over $20T in wealth for American households, equivalent to roughly 70% of American GDP in 2024. This is several times larger than the losses incurred during the crash of the early 2000s.”

So when would this happen?

Well, optimists hope, never: If AI companies succeed in quickly creating AGI, investors may not be putting enough in. But setting that aside, no one knows: It could be whenever the mood shifts, when investors go from worrying that they invested too little to investing too much; or it could be when a series of financial returns suggests that the promised payouts aren’t coming as quickly as needed.

For her part, Morgan Stanley’s Shalett said her staff was “starting to watch” for indications of a bursting bubble. “We’re a lot closer to the seventh inning than the first or second inning,” she predicted.

The fact is that no one knows what will happen or when. Yet, to make up your mind about when to sell, you could listen to Joseph Kennedy Sr., JFK’s father.

Kennedy allegedly sold his stocks in 1929, anticipating a crash and saving his family a fortune. When asked how he knew to do that, Kennedy said it was because he knew there was a bubble.

“How did you know?” his stockbroker allegedly asked.

“You know you are in a bubble,” Kennedy supposedly replied, “when the shoeshine boy starts giving you stock tips.”